Stop Housing Speculation with Math

Speculation in the real estate market has long been a problem for Canada [1]. There have been various reports and analysis on this topic [2] [3] [4], and different policies have been proposed and implemented, including the Non‑Resident Speculation Tax (NRST) in Ontario in 2017 [5], the Empty Homes Tax in Vancouver in 2017 [6] and the B20 Stress Test in 2018 [7]. But none of these seem to have a lasting effect, with affordability worsening by the day [8] and home ownership out of reach for millions of families. This has a negative impact on people’s quality of life and will hurt the long-term competitiveness of our economy [9].

The problem our major metropolitan has become hot spots for real estate speculation is not just because lives in those cities are desirable, but more because real estate investment in those cities are desirable. Several top reasons are:

- Politically stable.

- A free market where capital can easily flow in and out.

- Population growth and tight rental market.

Therefore, the supply and demand problem that drives housing price up can never be addressed by simply building more homes, because they take too much time and any supply created will be very quickly absorbed by new money flowing into the market. The key is to control the demand and especially speculative demand, whether foreign or domestic.

Speculators buy investment properties for a return, and the key to stop housing speculation is to make that return less appealing. To understand how to achieve that, we first need to understand how investment properties make money. Below is a diagram that outlines the inflow and outflow of cash, and the appreciation of an investment property:

Based on this, we can build a simple mathematical model that emulates the cashflow of an investment property with 1 million dollars of purchase price in a 25 years monetization period around these factors. With this model, we can then run sensitivity analysis to find out which are the deciding factors for an annualised Return of Investment (ROI), and implement policies to calibrate them, which ultimately leads to a calibration of ROI.

The key idea here is — rather than coming up with individual policies that target at different things such as foreign buyers or vacant properties, we look directly at the ROI and try to design a framework of inter-connected policies that would work together to keep ROI for investment properties locked in a reasonable range, thus to stop highly leveraged, short-term speculators but encourage owner-occupied buyers and long-term investors. This will hopefully provide a new way to frame the housing speculation problem and inspire new discussions and ideas.

The method for this simple sensitivity analysis is to choose 3 levels for each factor, low — base — high, and run the cashflow model with them. In each iteration, we only vary the selected factor while fix the others. We choose annualised ROI after 5 years as an indicator because that’s typically when a speculator will sell his/her investment property.

The factors and ranges of factors used here are (low — base — high):

- Down payment: 20% — 30% — 40%

Range to emulate down payment required for regular mortgage, and a potential down payment increase. - Mortgage rate: 1.5% — 2.75% — 4%

Range to emulate current low rate environment, back to normal and a potential hike. - Annual housing price increase: 5% — 10% — 15%

Range to emulate a normal growth, high growth (GTA/GVA last 10 years average) and a very high growth (hot markets) - Transaction fee and tax: 6% — 10% — 14%

Range to emulate normal fee plus a potential higher capital gains tax rate. - Property tax rate start: 0.5% — 1.25% — 2%

Range to emulate Toronto/Vancouver, some smaller cities, and a potential holding tax on investment properties. - Property tax increase per year: 5% — 7.5% — 10%

Range to emulate normal to high property tax increase per year. - Rent start when the property was purchased: 1500–2500–3500

Range to emulate low to high rent. - Rent increase per year: 2% — 6% — 10%

Range to emulate normal to high rent increase per year.

Maintenance is assumed to have a fixed start of $500 and increase by 3% per year.

Insurance is assumed to have a fixed start of $800 and increase by 10% per year.

Vacancy rate is assumed to be 10% per year.

Below is the Tornado chart of the sensitivity results. The base case with the yardstick centres around 20% annualised ROI and the bars indicate the range of ROI from low/high cases for each of the factor:

- The biggest bar, without any surprise, is the annual price increase. The more housing price rises per year, the more annualised ROI a speculator will have. However, in our free market, this cannot be directly controlled by policy makers. But still, it shows how much difference a 5% and a 15% yearly price increase can make to the ROI. Therefore, it makes housing speculation a self-fulfilled prophecy. As long as housing price keeps going up at a high rate, investment properties will attract more speculators and more speculators further push the housing price up. The only way to bring the price down is to bring the price down.

- The second biggest bar, is the down payment. Real estate investment is a game of leverage, and any policy that fails to address this will likely fail, too. The most direct way to stop housing speculation is to tighten the mortgage market, for example, increase down payment from 20% to 40% for investment properties — which is the exact same policy implemented in New Zealand by its central bank in early 2021 to clamp down speculation [9]. Down payment for first time homebuyers can be kept at current levels.

It is also important to consider bringing credit unions and private lenders under OSFI regulation and extend the B20 stress test rules to these financial institutions, too. This stops speculators from by-passing existing rules and protect the stability of our financial system. A Reuters report in 2019 claimed that this idea was being discussed by the federal government [11] but Finance Minister Bill Morneau later said it was not considered [12].

Meanwhile, strong actions need to be taken to crack down mortgage fraud. The 2015–2017 case for Home Capital Group (HCG), one of Canada’s largest alternative lenders, had greatly shocked the market. Brokers were found to submit false loan documents, such as inflated income statements, to help their clients qualify for mortgages [13] [14]. It is possible such practices exist in other financial institutions and they pose as a great threat to the stability of our financial system.

Another policy that needs to be seriously considered is to put more strict rules on using HELOC for down payment to buy investment properties. This helps to level the playing field between speculators with properties and first time homebuyers. - Rent is how speculators generate cashflow from investment properties. To grow our economy, inflow of immigrants will continue and the rental market will continue to be tight. Speculators can easily exploit renters and pass on any expenses or tax to them. Therefore, any policy package aims at stopping housing speculation needs to include terms to protect renters.

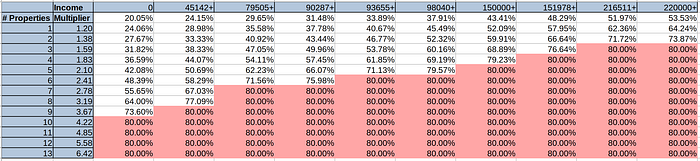

This can be done by implementing a Rental Income Guidance Tax (RIGT) for landlords and combined with tax deduction for renters. This tax system would apply a multiplier for all rental incomes. For example, with a multiplier of 1.15, a speculator reports 2500 * 12 = 30000 rental income, and when filing for tax, this will be counted as 30000 * 1.15 = 34500 on top of other income. The tax collected will be returned to the renter through tax deduction when reporting rental expense. This prevents tax evasion and helps renters to have more savings towards down payment and home ownership.

The multiplier should increase exponentially with the number of investment properties and personal income, to force speculators with many investment properties to free up resources to others. For example:

- This table shows the effective tax rate when combined with income brackets (using Ontario income tax brackets here). For example, if a speculator owns 4 investment properties and his/her annual income is $94,000, his/her effective marginal tax rate for rental income is 1.83 * 33.89% = 61.85%. The tax is capped at 80%.

In this way, a retiree A who depends on his 2 properties’ rental income for retirement will see his effective marginal tax rate increased only from 20% to 27%, which is not too much. While a speculator B with a $230,000 annual income who has been hoarding houses will very quickly see her effective marginal tax popping up from 53% to 80%. This, in combination with an Investment Property Special Tax (will be discussed later), will greatly increase costs for high earners with multiple properties and force them to sell to first time home buyers and owner-occupied buyers. This tax should be exempted for people who are renting out part of their primary residence, as a way to help them paying off their own homes.

This tax is also difficult to circumvent. Speculators cannot “gift” their properties to low income direct relatives because that in Canada is considered a capital gain and is subject to capital gain tax. They cannot use low income relatives’ names to buy homes either because those relatives will not qualify for a high amount of mortgage due to the B20 stress test (this also shows it’s important to bring alternatives lenders under B20).

Rent control programs can be lifted as it seems to be less effective and lead to renovications [14].

Furthermore, currently mortgage interest for investment properties can be used to deduct from rental incomes. This need to be partially removed, for example, making only 50% of mortgage interest applicable, to make this tax more effective. - Transaction fee and tax reflects the expense incurred when selling the property. A way to stop speculators is to increase the tax inclusion rate on the capital gain of selling investment properties, for example, from the current 50% to 75%. Similar ideas have been touted by the then Ontario Finance Minister Charles Sousa in a letter to Canadian Finance Minister Bill Morneau back in 2017. [16]

Different brackets could be implemented, too — for example, properties held for 0~5 years with 100%, 5~15 years with 75% and 15+ years with 50%. This is to encourage long-term investors who wants to grow their investment with Canada and also protect those who relies on their investment properties for retirement. Tax generated can be used towards providing housing to and help low income communities. - Property tax increases the holding cost and decreases the cashflow for investment properties for speculators.

An annual 1% Investment Property Special Tax (IPST) for investment properties can be implemented on top of the existing property tax, in combination with the Rental Income Guidance Tax discussed above to prevent speculators form passing this tax onto renters. This tax should be non deductible, and it will squeeze the cashflow for highly leveraged speculators and force them to put their properties on the market, which increases supply and benefit first time home buyers. Again, the tax collected can be directed to build more affordable housing and social housing for low income communities. - This could be to many people’s surprise, but mortgage rate is the least deciding factor here. This could be because the range of mortgage rates we can effectively tweak is quite limited due to economical constraints (here using 1.25% to 4%), compared to the 1990s when rates was as high as 14% [17].

This is actually a very good news for policy makers, because it means by implementing the above, we can still keep a relatively low interest rate to stimulate the economy in other sectors.

Summary

To deter future speculators, thus decrease housing speculative demand:

- Increase down payment for investment properties from 20% to 40%.

- Increase capital gains inclusion rate for investment properties from 50% to 100% (holding 0~5 years before sale), 75% (5~15 years) and 50% (15+ years).

- Put all credit unions and alternative lenders under OSFI and B20.

To gradually squeeze the cashflow for highly leveraged speculators and force them to sell, thus increase housing supply:

- Apply a Rental Income Guidance Tax (RIGT) for landlords and provide tax deduction for renters for all investment properties.

- Apply a Investment Property Special Tax (IPST) per year on top of property tax for all investment properties.

Thoughts on the Future of Real Estate Investment

We need to be very clear about one thing — the goal here is not to stop real estate investment. Before coming up with any policies, we need to admit that real estate is an important and integral part of the economy and it helps numerous upstream industries, such as building and home renovation to create jobs. The goal is to bring the ROI of real estate investment to a more reasonable level, on par with other investments such as RRSP and Mutual Funds, so that it is less appealing to speculators. This helps to redirect excessive money to either invest in our own people, our business sector, or spending which will in turn help our small business to grow and create more jobs.

With more data and a more complicated model, the ROI of investment properties can be calculated and closely controlled by RIGT and IPST. This gives us the flexibility to review and calibrate them on a region by region and year by year basis. If we want to encourage housing market activity in certain remote areas, we can tune these two knobs to increase the ROI. If the housing market is slowing down too much and hurting the economy, we can also tune these two knobs that year to stimulate activity. In the long-term, we use this model to maintain ROI of investment properties in a reasonable range.

This system helps to generate more savings for renters through tax deductions and bring home ownership back in reach for them. And with more listings from squeezed highly leveraged speculators, more owner-occupied home buyers can finally have their dream home, whether they’re first-time home buyers or looking for an up-size with their growing family. It helps to maintain long-term healthiness and stability of our housing market and avoid boom — burst cycles and potential catastrophic consequences.

Meanwhile, to make sure we’re building enough rental housing, we should encourage people to invest in purpose-rental REITs (Real Estate Investment Trusts), by giving dividends from REITs special tax incentives — instead of becoming landlord themselves. In this way, REITs will lead the way to build more homes, which also helps bolstering our building industry. We will apply a similar idea of ROI control to these REITs to prevent price gouging and renovication. I will discuss in details how this works in a follow-up article.

While speculators are gradually squeezed out of the market, real estate investors who want to grow their investment together with the growth of Canada will be encouraged and they will enjoy a rewarding steady and long-term return.

References:

- https://en.wikipedia.org/wiki/Canadian_property_bubble#:~:text=The%20Canadian%20property%20bubble%20refers,to%20337%25%20in%20some%20cities.

- “Swiss bank UBS says Toronto has 3rd biggest housing bubble in the world” https://www.cbc.ca/news/business/ubs-toronto-housing-bubble-1.5746432

- “Housing Market Assessment — Canada and Metropolitan Areas” by CMHC https://www.cmhc-schl.gc.ca/en/data-and-research/publications-and-reports/housing-market-assessment

- “Unbreakable Canadian Housing?” by BMO https://economics.bmo.com/en/publications/detail/9b7433d3-ae19-4687-a26f-747e3093b35b/

- “Non‑Resident Speculation Tax (NRST)” in Ontario https://www.fin.gov.on.ca/en/bulletins/nrst/

- “Empty Homes Tax” in Vancouver https://vancouver.ca/home-property-development/empty-homes-tax.aspx

- “Residential Mortgage Underwriting Practices and Procedures Guideline (B-20)” by OSFI https://www.osfi-bsif.gc.ca/Eng/fi-if/rg-ro/gdn-ort/gl-ld/Pages/b20-nfo.aspx

- “‘Saving For A Down Payment Has Never Been Worse,’ Says National Bank Of Canada” https://www.huffingtonpost.ca/entry/saving-down-payment_ca_601afd00c5b67cdd1a74fb7b

- “While the world is in the midst of a tech revolution, Canadians bet on real estate” — https://financialpost.com/news/economy/while-the-world-is-in-the-midst-of-a-tech-revolution-canadians-bet-on-real-estate

- “New Zealand Clamps Down on Property Investors as Prices Soar” — https://www.bloomberg.com/news/articles/2021-02-08/new-zealand-to-clamp-down-on-property-investors-as-prices-soar

- “Exclusive: Canada mulls measures to curb private lenders’ growth” https://www.reuters.com/article/cbusiness-us-canada-housing-privatelende-idCAKCN1PJ1YV-OCABS

- “Stress tests on private lenders not being considered, Morneau says” https://financialpost.com/real-estate/mortgages/stress-tests-on-private-lenders-not-being-considered-morneau-says

- “In Home Capital’s mortgage mess, blame the ‘unlucky’ brokers” https://financialpost.com/news/fp-street/in-home-capitals-mortgage-mess-blame-the-unlucky-brokers

- “Home Capital Group Inc’s probe into alleged fraud by mortgage brokers widens” https://financialpost.com/news/fp-street/home-capital-group-incs-probe-into-alleged-fraud-by-mortgage-brokers-widens

- “How Toronto landlords use renovictions to force out tenants” https://nowtoronto.com/news/renovicted-toronto-rental-housing

- “Canada will work with provinces on housing affordability: spokeswoman” https://www.reuters.com/article/cbusiness-us-canada-economy-housing-idCAKBN16S1M8-OCABS

- “Interest rates and exchange rates” by Statistics Canada https://www150.statcan.gc.ca/n1/pub/11-210-x/2010000/t098-eng.htm

Disclaimer:

This article and everything included, for example — models, data or program code, are provided for general informational purposes only. Information may be changed or updated without notice. All information here is provided “as is”, with no guarantee of completeness or accuracy. The author assumes no responsibility for consequences resulting from the use of the information here.

This article follows the Creative Commons license.